.avif)

Today, we’re diving into the structural shift happening in digital assets—why Bitcoin’s dominance is nearing its peak, how stablecoins and tokenization will reshape the market, and why the next era belongs to fundamentals over speculation.

The digital asset space is undergoing a structural shift. The cycle is broken. I foreshadowed this phase in June of 2024 in my 2024 Outlook, where I explored the fundamental shifts that could occur in a post-Gensler era. In particular, I wrote that:

“The most meaningful graduation from being speculative assets to investable assets for the wider digital asset space beyond Bitcoin’s digital gold thesis occurs the moment tokens can accrue value without being at odds with regulators. While part of the debate is whether or not digital assets are commodities or securities, the other meaningful debate is how crypto assets can be compliant in a way that does not go against the underlying technology.”

Despite Trump’s victory and sweeping regulatory changes, the market is having one of its worst stretches and appears to be charting a new course, away from its traditional four year cycle. We are at a unique juncture for the digital asset market, where all of the following appear true to me over the next twelve months:

- Bitcoin has become the consensus trade, and Bitcoin dominance as a portion of the crypto ecosystem is likely nearing its all-time high for the remainder of history over the next 3–6 months.

- Bitcoin will nevertheless continue to compound growth year over year.

- The wider digital asset space will continue to undergo a period of crisis over the next six months.

- The wider digital asset space will outperform Bitcoin in the decades thereafter.

The reason for this prediction is twofold.

Long Term: From Financial Nihilism to Utility

We are approaching the zenith of financial nihilism, exemplified by phenomena such as Trump coin, Milei's Libra, and the billions lost in memecoin ventures. As momentum has now firmly broken and most fundamentally unsound digital assets have declined by 90–99.9%, their return seems unlikely. Retail investors, as a result, are burned out. The speculative games have proven to be zero-sum and rigged, leaving the market fleeced and unwilling to participate any longer.

The next marginal buyer is Wall Street. Digital assets with strong fundamentals and revenues will be bid up by institutional buyers before any other digital asset is likely to draw institutional interest. It follows that retail, eager to make money, will flock toward whatever is appreciating, compounding the fundamental soundness premium further (as we see with the Mag 7 in equities).

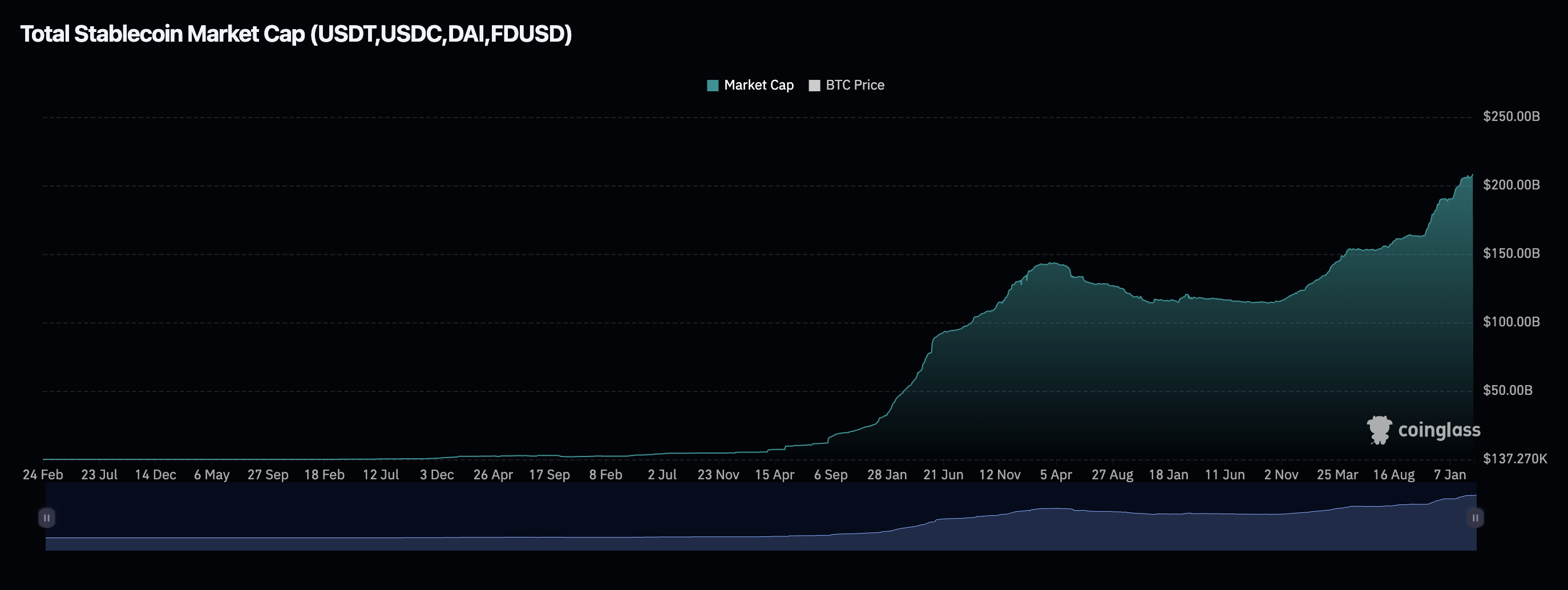

The big innovation that the economy, government, and Wall Street are ready for is stablecoins—for those not familiar, fiat currency that has been moved onto the blockchain (tokenized dollars, euros, etc.). Already today, stablecoins have onboarded more than 1% of the entire M2 money supply and are growing at a breakneck pace —even in bear markets.. However, it will not end with mere transactions in USDT or USDC.

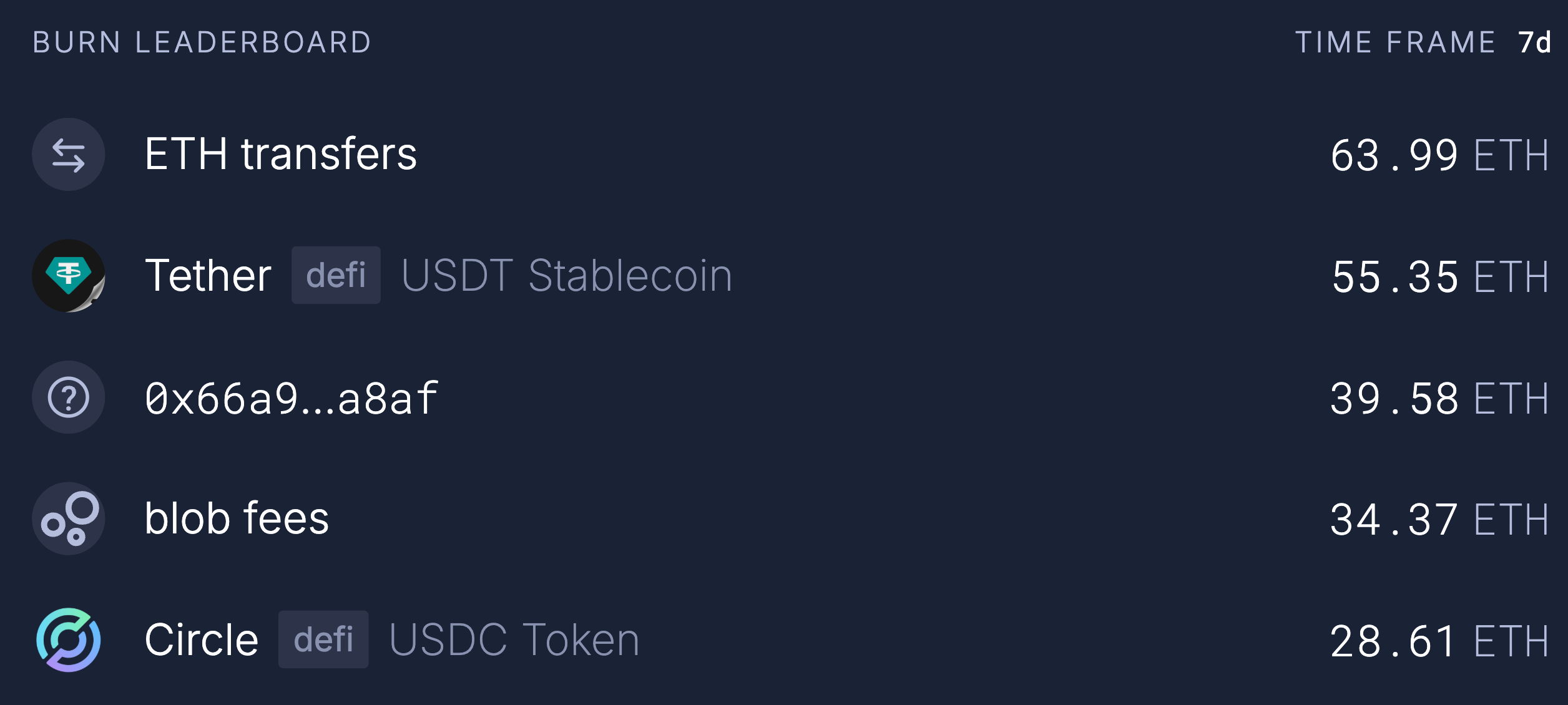

There will be increased demand for financial primitives like lending, borrowing, swapping, etc., of on-chain assets, driving material revenue toward leading DeFi protocols. Already today, stablecoins are the largest revenue contributors on the Ethereum blockchain, where Tether and Circle combined lead the list of fee sources. As the world continues its reliance on and use of stablecoins to save fees and time, the tokenization of most other financial assets follows closely.

Stripe, the world’s largest privately-held fintech company, raved about stablecoins in their 2024 annual letter, likening them to room-temperature superconductors for the financial services industry. They wrote:

“Stablecoins have four important properties relative to the status quo. They make money movement cheaper, they make money movement faster, they are decentralized and open-access (and thus globally available from day one), and they are programmable. Everything interesting follows from these characteristics.”

Today, stablecoins are primarily used for international remittances and as one of the fastest ways for those living abroad to gain exposure to U.S. dollars. However, stablecoin activity remains largely limited due to regulatory constraints, which the current administration is re-writing as we speak.

The even bigger innovation the world is likely not quite ready for yet—but which will yield some of the most outsized returns—is the intersection of crypto and AI. As AI agents gain access to a fully digitally native financial suite, they will become truly autonomous participants in our economy. The first step to unlocking this milestone, however, is onboarding the majority of online commerce onto stablecoins.

Short-Term Challenges: The Regulatory Gap and Catalyst Vacuum

Despite all these promising forces, regulation takes time. Until laws are drafted, signed, and adopted, it is unlikely that we will see fintech hit the go-button and roll out stablecoins at every checkout, instantly bringing every American on-chain overnight.

We are, in a way, stuck in an awkward in-between spot, where the “Trump trade” is behind us, macro risk-off weighs heavily on the market, and yet the actual meaningful changes will take longer than a simple Executive Order signing. While the market is starved for near-term catalysts, flows remain lopsided toward sellers.

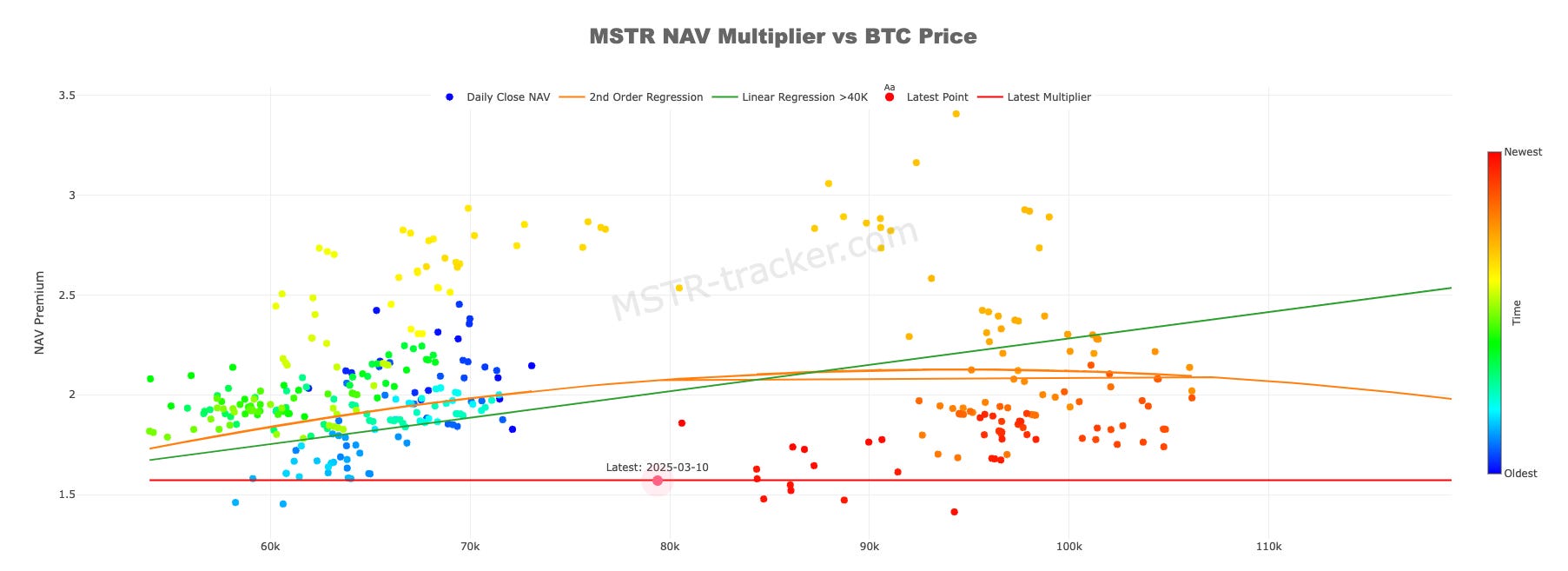

Michael Saylor—the man propping up the market with over $20bn worth of purchases since November—is slowly running out of ammo. MSTR’s premium to NAV is one of the lowest in the last 12 months. I highlighted this in my December write-up, when the premium was near 2.5x. Today, the premium is down to 1.5x, a material decline in just three months. (ELI5: Saylor has been issuing and selling MSTR shares to finance Bitcoin purchases. This generates “yield” as he puts it as long as he sells the shares at a premium—however, that premium is now nearly depleted.)

Without Saylor manning the gunships, the market relies on real fundamentals. Unfortunately, as I have pointed out for years, 95% of assets are massively overvalued or even vaporware. VCs and Founders alike know this. As a result, their tokens, which are vesting daily, are heading for the exit, adding material recurring sell pressure.

Unfortunately, the market is punishing the other 5%—the fundamentally sound digital assets with millions of users and earnings—just the same. This may seem counterintuitive:

How can a decentralized exchange or lending market in a high-growth industry decline to 2–4 PE ratios or even sometimes trade at book value?

The answer lies in the composition of market participants pre-Wall Street:

- Retail traders—who trade purely based on sentiment. They will sell AAVE at a single-digit P/E ratio for the same reason they buy Fartcoin on the way up. They react emotionally to price movement, with no fundamental thesis.

- Quant traders and funds—who trade based on historical correlations. Crypto follows cyclical, highly correlated patterns: few tokens appreciate in a bear market, and even overvalued projects continue rising in a bull market. If 95% of tokens experience net outflows and decline, statistical arbitrage strategies will short or sell the remaining 5%, expecting mean reversion due to historically high correlation.

- Crypto VCs—who raised funds between 2017–2021 and are now 4–9 years into their vintage, pressured to deliver returns to LPs.

- Crypto-native liquid funds—which are not seeing inflows. If anything, many are facing outflows, as Bitcoin ETFs have diverted much of the institutional demand.

What you are left with is an awkward vacuum. While BTC is near all-time highs, the average crypto asset is down 50–99%, including Ethereum and Solana.

The largest resignation in the industry’s history is unfolding.

People are giving up, announcing on X that they are selling everything and leaving. The market has been thankless and treacherous for anyone outside of Bitcoin.

Even I have questioned whether running a liquid fund makes sense in these conditions.

But to me, it is undeniable that stablecoins will be globally adopted in the next 2–3 years. As a result, the underlying infrastructure will experience exponential revenue growth.

This is an asymmetric opportunity for those patient over the next six months—one we have not seen in four years.

How am I positioning our liquid fund for this environment?

In mid-February, we materially de-risked our portfolio after the market broke long-term momentum structures.

From here forward, we will take a strategic liquid venture approach, searching for the most fundamentally sound projects that will benefit from:

- Stablecoin proliferation

- AI integration into finance

The entire DeFi industry has a combined market cap of just $75bn—half the size of Uber.

In fact, every single token outside the Top 10 has a cumulative market cap of just $250bn. Our belief is not only that this segment will evolve into a $10TN+ economy (40x growth), but even more so that the market has violently mispriced its assets. Currently, perhaps $200bn in value is tied up in vaporware, while only $50bn or so is allocated to projects that are truly defining the technology. As capital rotates, we expect this imbalance to correct, driving exponential upside for the assets with real fundamentals.

At this juncture, I believe the era of trading has passed, and the time to invest has come. The noise of sentiment has likely cost most active funds—ourselves included—more upside than it has helped prevent downside. Going forward, I will be spending less time looking at price and more time focusing on value. When those two meet or come close, I will be a buyer, regardless of daily volatility.

My belief is that the right portfolio construction—a blend of 20–40 assets, accumulated amidst the coming sell-off, with exposure to both public and private offerings—will materially outperform not only Bitcoin but most asset classes.

The Four Year Cycle is Broken

Why?

Because mature industries don’t rely on four-year hype cycles—growth is constant. No matter how grim the market outside of Bitcoin looks today, and though it may get worse first, we are nearing a point where stablecoins will be used daily by everyone, whether they realize it or not.

And then? Everything tokenizes.

The first mover to watch is Coinbase, which recently announced plans to launch a tokenized version of its stock. When this succeeds, it will set the precedent for a future where all financial assets can be traded 24/7, instantly, globally, and used as collateral.

The $100bn on-chain economy will become a $10TN+ industry.

Nobody said it would be easy. But getting the stablecoin and tokenization trade right will make all this volatility worth it.

Disclaimers:

This is not an offering. This is not financial advice. Always do your own research. This is not a recommendation to invest in any asset or security.

Past performance is not a guarantee of future performance. Investing in digital assets is risky and you have the potential to lose all of your investment.

Our discussion may include predictions, estimates or other information that might be considered forward-looking. While these forward-looking statements represent our current judgment on what the future holds, they are subject to risks and uncertainties that could cause actual results to differ materially. You are cautioned not to place undue reliance on these forward-looking statements, which reflect our opinions only as of the date of this presentation. Please keep in mind that we are not obligating ourselves to revise or publicly release the results of any revision to these forward-looking statements in light of new information or future events.

March 11, 2025

Share